ETP just launched in Switzerland")

Earlier this week, JPMorgan published a global markets strategy note that points out money has flowed out of gold and into bitcoin since October, and predicts this trend will continue over the medium to longer term.

The easy conclusion is that investors are finally understanding that bitcoin is a superior future store of value to gold, and are rotating out of one and into the other.

I’m not convinced that’s what we’re seeing. I agree with the analysts, though, that inflows into bitcoin will continue to increase, but not because investors are changing their minds. There’s something else going on.

In and out

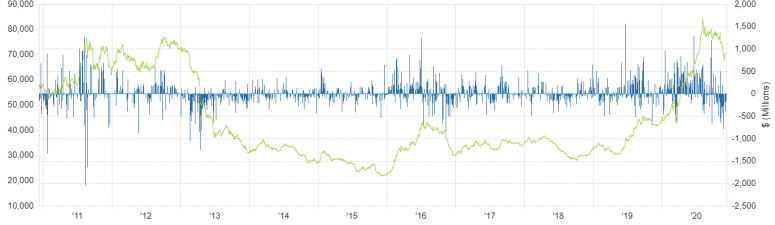

The main gold exchange-traded funds (ETF) are losing funds – that much is true. SPDR Gold Shares (GLD) and iShares Gold Trust (IAU) have seen outflows of over $4.4 billion in the past month alone, according to FactSet. The Grayscale Bitcoin Trust, however, which trades under the symbol GBTC and is managed by Grayscale (owned by DCG, also parent of CoinDesk), has seen inflows of over $1 billion in the same period, according to the latest 8-K filings.

But the two trends are not necessarily correlated.

Gold fund outflows are not that unusual, as the below chart shows.

What’s more, the latest movements come after a phenomenally successful few months – since the beginning of 2020, GLD and IAU saw inflows of over $25 billion, marking the strongest year for inflows over the past decade. Even with the latest outflows, it has been a very good year for gold funds.

The gold price has responded, delivering 35% performance between Jan. 1 and its peak in August. What we could be seeing is a simple rebalancing as investors lock in profits to reinvest elsewhere.

Add to that a change in risk-off sentiment, as investors see less need for “safe haven” investments given positive vaccine news and the potential for strong growth next year, not to mention confidence the U.S. Federal Reserve will keep the markets happy, and you have an unsurprising shift away from gold. That does not mean that institutions are replacing their positions with bitcoin.

Growing confidence

We do know, though, that institutions are getting interested, and a growing number are becoming active in the crypto market. These institutions are not the only drivers of bitcoin inflows, however.

The GBTC trust mentioned above is only available upon issuance to accredited investors, who can sell on the over-the-counter (OTC) market after a six-month lock-up period. The listed price carries a premium to the underlying value, which represents the strength of retail demand for bitcoin exposure. In what is known in the market as the “premium trade,” accredited investors that sell into the market after the lock-up capture both any bitcoin appreciation and the premium, and often reinvest all or part of the proceeds into new trust shares. Without strong retail demand, the GBTC premium would dwindle.

Retail investors are probably behind some of the outflows in gold ETFs, and some are probably rotating into BTC. But there’s a bigger story unfolding.

It’s the generational shift.

The sands of time

This week, financial advisory firm deVere released the results of a survey of over 700 of its millennial clients, which showed two-thirds of them prefer bitcoin to gold as an investment. This means any new savings entering the market may be almost 70% more likely to be put in bitcoin than into gold.

This makes intuitive sense: Millennials are more comfortable with technology than their elders, and can probably grasp the potential more easily. And a Pew report last year showed younger Americans are less likely to trust institutions than older generations. Recent events are likely to have weakened this trust even further, at a time when the savings rate of those millennials and Gen Z-ers fortunate enough to have kept their jobs through the pandemic is increasing.

A New York Times article from earlier this year presented the millennial generation as focused on early retirement, which will concentrate their attention on long-term value that cannot be inflated away.

All this makes young people more likely to invest in inflation-resistant assets, yet less likely to invest in gold.

For one thing, it is difficult for retail investors to actually hold gold. Sure, they can buy shares in a gold ETF, but that implies more centralized control and institutional vulnerability than a self-custodied bitcoin investment. And in an environment of weakened trust in the current system, self-custody of bitcoin is a much easier solution than is self-custody of gold.

Old and new

So we are likely to have significant new demand for bitcoin as a portfolio investment coming in from younger retail investors, at a time professional investors are also taking notice. It’s not just bitcoin fundamentals at work. Many professional investors will be interested in bitcoin investment precisely because of this potential growth narrative – other people wanting bitcoin is enough to make them want bitcoin.

And, unlike gold, growth in demand for bitcoin does not affect its supply, which feeds the narrative loop even more.

Throw in the dwindling rate of new bitcoins entering the system, and the demand-supply dynamics could entice even traditional investors to take an interest. This week we saw Massachusetts Mutual Life Insurance Co. – yes, an insurance company – invest $100 million in bitcoin.

This does not mean that gold investment is over. Gold’s role as a store of value is well entrenched in investment lore, and even forward-thinking and open-minded investors and advisers recommend that bitcoin complement the precious metal rather than replace it.

But a new generation of investors is starting to rewrite the rulebook. For now, the impact on gold flows is negligible, and we will see funds rush into industry ETFs when markets get wobbly and the commodity price starts to move up again. But demographics and sentiment are two powerful forces that, working in tandem, can move mountains – even those made of gold.

Balancing act

Software firm MicroStrategy’s enthusiasm for bitcoin is now industry lore. The company was the first to publicly acknowledge putting all of its excess treasury in the crypto asset, and its CEO Michael Saylor has become a crypto celebrity with his conviction and insight, even making CoinDesk’s Most Influential list this year.

This week he went even further: Not content with the $475 million already invested in the asset, MicroStrategy issued $650 million of convertible bonds (which was initially going to be $400 million and then got raised to $550 million and then got raised to … you get the picture), the proceeds of which will go to buy more bitcoin.

Is he nuts? Or is this the corporate treasury management of the future?

In my opinion, possibly both. Bitcoin is a relatively volatile asset, and corporate treasury is not the place to take risks. Citi seems to agree because it downgraded its recommendation on MicroStrategy stock to a “sell” this week. At time of writing (Friday afternoon), the share price has fallen almost 15% over the week.

But bitcoin is actually a potentially excellent corporate treasury asset. Ria Bhutoria and Tess McCurdy of Fidelity Digital Assets as well as Jeff Dorman of Arca funds wrote great pieces this week detailing this point.

Ria Bhutoria and Tess McCurdy of Fidelity Digital Assets in which bitcoin can mitigate typical corporate treasury risks. For instance, balance sheets are often exposed to liquidity risk, in which a company does not have enough liquid assets to meet debt payments and so has to sell less-liquid assets at unfavorable prices. Holding bitcoin instead of these less-liquid assets frees up cash in order to satisfy obligations, as bitcoin can be used as collateral on many lending platforms.

Foreign exchange risk leaves a company vulnerable to fluctuating conversion rates and fees – bitcoin could serve as a “bridge asset” on the balance sheet, moving in and out of currency pairs at a lower cost.

Jeff Dorman of Arca funds that holding cash on the balance sheet for large corporations is onerous, usually requiring several accounts, limited banking hours, wire fees as well as the need to earn a yield on cash holdings. He also hinted, and this could be fun, that activist investors could soon start pressuring companies to diversify treasury holdings with bitcoin.

I’m interested in the potential use of bitcoin as collateral for working capital management. Ria and Tess touched on this, but I think it could go even further, eventually giving rise to a new type of repo market.

Yes, bitcoin fluctuates in fiat terms, and company financing needs are in fiat terms – but bitcoin’s bearer nature combined with its ease of transfer and the work being done on its smart contract functionality, as well as the growing support for bitcoin custody from financial institutions, point to some interesting developments on this use case in the years to come.

Anyone know what’s going on yet?

As the specter of no deal on Brexit looms ever closer, and stimulus talks in the U.S. are mired in a political stalemate, markets showed some signs of nerves this week – not nearly as much as the dire outlook warrants, however, which is itself becoming the new normal.

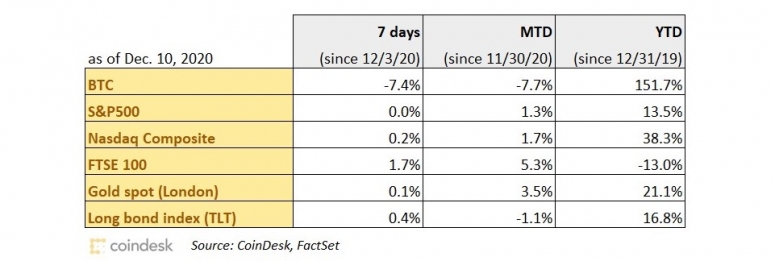

Interestingly, BTC’s weak performance so far this month does not seem to have damped spirits in the industry. The year-to-date performance is still higher than more traditional alternatives, institutions continue to demonstrate interest and infrastructure development continues apace. In spite of this week’s dip, there still seems to linger a feeling of accumulation.

Chain links

Continuing with the idea I kicked off last week to list the professional investors and institutions talking about bitcoin in a separate section (because the comments are coming thick and fast these days), the following people/companies said some relevant things:

- An editorial in the Financial Times by Morgan Stanley Investment Management’s chief global strategist positions bitcoin as a potential substitute for the dollar as a global currency. “There are reasons to think this bitcoin rush has deeper roots.”

- Bridgewater Associates founder Ray Dalio, who has spoken out against bitcoin in the past, has softened his stance, and said in an AMA on Reddit this week that he thought bitcoin and other cryptocurrencies had “established themselves” over the last 10 years and were interesting “gold-like asset alternatives.”

- In a long Twitter thread, investor Raoul Pal riffed on the potential value comparisons and growth drivers for BTC and ETH: “My hunch is BTC is a perfect collateral layer but ETH might be bigger in market cap terms in 10 years.”

- Mohamed El-Erian, chief economic adviser for €2.3 trillion fund manager Allianz, tweeted last week he had sold bitcoin after holding for two years, and that his decision was “not based on any deep analysis.”

- German media giant Bertelsmann has invested in a crypto fund managed by venture firm Greenfield One.

In other news:

An insurance company founded in 1851, Massachusetts Mutual Life Insurance Co., invest $100 million and $5 million in an equity stake in crypto fund manager NYDIG. TAKEAWAY: You read that right: An insurance company has invested in bitcoin. This is the first large insurance company to do so, as far as I’m aware, and the scale of the investment – only 0.04% of the general investment account, and is just a “first step,” according to the company – gives an inkling into the size of the potential funds should other insurance companies start to follow suit.

Fidelity Digital Assets is entering the crypto lending business, albeit indirectly, allowing its institutional customers to pledge bitcoin as collateral against cash loans in a partnership with crypto lending firm BlockFi. TAKEAWAY: The growth of the lending business is worth keeping an eye on, as it represents a maturation of the market as well as a sign that liquidity will continue to improve. More than that, the growing awareness of the advantages of bitcoin as a collateral asset is likely to lead to new types of infrastructure emerging, as well as new use cases for bitcoin and other cryptocurrencies.

According to sources, Spanish bank BBVA will soon launch cryptocurrency services, based out of Switzerland. These services will include trading and custody. TAKEAWAY: If true, this would be a major bank (second-largest in Spain, 17th in Europe) validating cryptocurrencies as a tradable asset. The bank has for some time been regarded as one of the most “digital” and forward-looking in Spain (a few years ago I heard then-chairman Francisco González say: “We are not a bank. We are a technology company.”), and has been experimenting with blockchain applications since at least 2015, which arguably gives it a head start. If BBVA launches crypto trading and custody for its clients, other banks are sure to follow.

According to Michael Sonnenshein, managing director of crypto fund manager Grayscale Investments (owned by DCG, also parent of CoinDesk), a growing number of accredited investors are investing in the company’s ether fund (ETHE) even before investing in the standard industry “on-ramp” of their bitcoin fund. TAKEAWAY: This does more than hint at a growing sophistication in investors’ understanding of the different value propositions of ether and bitcoin. It also signals that investors increasingly grasp that the ecosystem is about so much more than seizure-resistant hard supply assets, and that native assets are in themselves technologies, each with its own strengths and potential. It will be interesting to see whether these investors remain exclusively focused on ether, or whether it will itself become an on-ramp for investments in Ethereum-based tokens and perhaps other protocols.

Germany’s second-largest stock exchange, Borse Stuttgart, has revealed that its Bison crypto trading app exchanged €1 billion (US$1.21 billion) worth of crypto assets so far this year. TAKEAWAY: This is a significant indication of retail interest, and the growth in the number of active users (180%, to reach 206,000), in an app that is more than two years old, hints at strong momentum.

Bitwise Asset Management announced this week that its 10 Crypto Index Fund is now available to U.S. investors as a public-traded cryptocurrency index fund under the symbol BITW. TAKEAWAY: It has only been trading for a few days, so it’s too soon to gauge what its liquidity will be. Its main competitor is Grayscale’s Digital Large Cap Fund. Like the Large Cap Fund, BITW is available to accredited investors at issuance and can be sold to the public after a 12-month lockup. Also like the Large Cap Fund, BITW trades at a premium to NAV – this premium has shot up since launch to almost 130% at time of writing.

Legacy bank involvement in crypto assets is gathering speed.

- Netherlands-based bank ING spoke publicly this week for the first time about the work done so far with Pyctor, a collaborative effort involving ING, ABN AMRO, BNP Paribas Securities Services, Citibank, Invesco, Societe Generale, State Street, UBS and others to develop custody and post-trade infrastructure for crypto assets.

- And Standard Chartered’s fintech investment unit, SC Ventures, and Northern Trust have announced Zodia Custody, a U.K.-based cryptocurrency custodian for institutional clients expected to begin operating next year.

- Standard Chartered has also gathered a group of crypto exchanges for a new digital asset trading platform tailored to the institutional market, according to sources.

TAKEAWAY: The entrance of legacy financial institutions into the crypto asset services business is no longer in doubt, and next year we will most likely see at least a handful offer these services to their clients. (Last week we reported that Spain’s BBVA will soon launch cryptocurrency services of crypto services). This will significantly move the needle on mainstream trust in crypto assets – if banks are offering these services, it must be legit, right? – and could lead to some bundling as banks make strategic acquisitions in the crypto industry. For some banks it will be a question of rapidly consolidating position and building ancillary services, for others it will be to try to catch up.

BitGo has added capital introduction services to its suite of white-glove crypto brokerage services. TAKEAWAY: This is another pillar in the emerging prime brokerage structure emerging in crypto markets. Capital introduction in crypto markets will serve more than merely to introduce institutional funds to fund managers; it will also be an opportunity to educate more institutional investors about crypto assets.

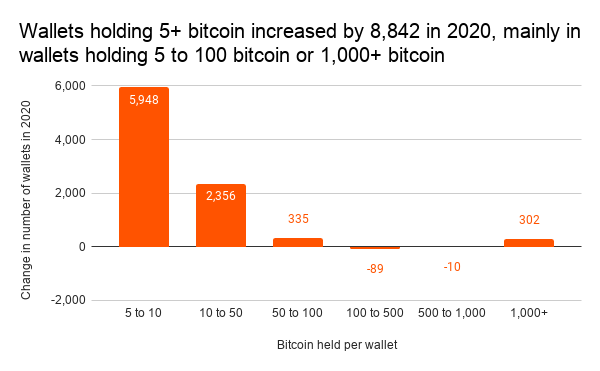

The number of bitcoin “whales,” or holders of over 1,000 BTC, has increased by 17% in 2020, according to blockchain forensics firm Chainalysis. TAKEAWAY: The industry likes to keep a track of this because it represents deep conviction and/or institutional stakes. A higher number of large holders does also introduce some centralization through concentration of wealth, and the risk that any one of these holders could sell, pushing the market down. But, the same analysis shows that the number of wallets that hold five to 10 BTC had increased by a considerable amount.

U.S.-based crypto exchange Bittrex Global has launched trading in tokenized stocks such as Apple, Tesla, Facebook and Amazon on its digital asset exchange. TAKEAWAY: You might wonder why investors would want to do that when they could use their traditional broker. But this offers a wider range of investment options for Bittrex users who might not have a traditional brokerage account, or who might not want to transfer funds. And, more importantly, it offers fractionalization of the shares, which could broaden their appeal to retail investors. Since Bittrex is not a large exchange (28th in spot volumes, according to CoinGecko), volumes in these tokenized shares is unlikely to be high – but it’s an intriguing step towards tokenization of assets on a broader scale, and could soon open up access to non-U.S. shares as well as other types of assets.

As further evidence the market for tokenized securities is quietly evolving, the innovation division of fund manager Arca has partnered with several crypto firms (Anchorage, Gemini, Komainu, Ledger, and TokenSoft) for custody of ArCoin, which represents tokenized shares in a SEC-registered fund that holds T-bills. TAKEAWAY: Choosing a range of custodians rather than just one offers clients a more flexible solution, and could boost interest among investors that are already clients of the selected companies. Even more interesting, though, is that a boring, staid investment (a high-grade bond fund) can be exchanged peer-to-peer on a blockchain platform. This could start to shift traditional investors’ perception that blockchain-based assets are risky and volatile, and open their minds to the versatility that tokenization offers. It’s a start, anyway.

Custody startup Curv is teaming up with Ethereum-based crypto wallet MetaMask to allow institutions to be able to invest in decentralized finance (DeFi) protocols with institutional-grade custody options. TAKEAWAY: The DeFi industry is growing fast but is still tiny by traditional asset standards. The attractive yields and growth potential of some of the assets have started to attract institutional attention, however, and initiatives designed to make it easier for professional investors to explore the space are emerging to support this. We’ll no doubt see more announcements like this in the months to come.

An Ethereum-based fund managed by Canadian investment fund manager 3iQ has completed an initial public offering for around $76.5 million the Toronto Stock Exchange (TSX), under the symbol QETH.U. TAKEAWAY: This is not available to U.S. investors, which will limit its liquidity, but the emergence of another listed ETH play signals the deepening maturity of the ETH market infrastructure overall.