ETP just launched in Switzerland")

Bitcoin (BTC) surged 6% Wednesday to a new all-time high price, clearing the key psychological threshold of $20,000 that had acted as a market ceiling in recent weeks.

“If history is any indication of future performance, some kind of pullback in the overall market confidence should appear sooner rather than later,” the Norwegian cryptocurrency analysis firm Arcane Research wrote Tuesday in a report.

In traditional markets, European shares rose and U.S. stock futures pointed to a higher open as investors cheered prospects for a vaccine rollout and more economic stimulus while awaiting an expected announcement from the Federal Reserve at 2 p.m. Washington time on the latest monetary-policy decisions.

Analysts at Deutsche Bank and Bank of America say the Fed might adopt “qualitative” guidance as a way of determining how long to maintain its stimulus-focused purchases of government bonds, ongoing at a pace of $120 billion a month. Led by Chair Jerome Powell, the Fed already has added about $3 trillion to its balance sheet this year, roughly three-fourths the amount of money previously created in the 107-year-old institution’s history.

Market moves

(Editor’s note: This is the third installment of First Mover’s recap of how the bitcoin market evolved over the course of 2020 and what it means for the future. Today we cover March and April, when the fast-spreading coronavirus began to take its toll on the global economy, sending markets into a tailspin and leading to an unprecedented financial response from governments and central banks around the world.)

It started off in late February as just another thread in the bitcoin market commentary. Global authorities were struggling to contain an unusually contagious and deadly virus outbreak from spreading beyond China.

Bitcoin, fresh off a five-month high around $10,500, racked up three straight days of price declines greater than 3% each. Initially, it seemed like no big deal in notoriously volatile digital-asset markets, especially since global stock markets were getting hit, too.

“There’s certainly a bit of fear in the bitcoin market, but it’s not anything close to the panic we’re seeing on Wall Street today,” Mati Greenspan, founder of the analysis firm Quantum Economics, which specializes in cryptocurrencies and foreign exchange, said Feb. 24. “Three percent is a very different figure for stocks and for bitcoin.”

What happened next was one of the swiftest and deepest sell-offs in the history of global markets, dragging down bitcoin to as low $3,850 by mid-March.

Which of course was followed by a dramatic push by U.S. lawmakers, the Federal Reserve, the swiftest and deepest sell-offs, Bank of Japan and authorities around the world to ply markets and the economy with trillions of dollars of stimulus money, bringing asset prices roaring back. By the end of April, bitcoin had more than doubled to about $8,600.

And that’s when the calls apparently started pouring into cryptocurrency startups from Wall Street. Bitcoin, whose ultimate supply is famously hard-capped at 21 million under the underlying blockchain network’s 11-year-old programming, had been cast as a potential hedge against central-bank money-printing and currency debasement, a modern and theoretically more portable version of gold.

“I’m getting calls from real big investors we’ve never seen before, saying, `roaring back,’” Michael Novogratz, CEO of the cryptocurrency firm Galaxy Digital, told CNBC on April 2.

Economists wrestled with the question of whether deflationary forces might overwhelm any inflationary impulse, based on the expectation that coronavirus-related lockdowns would decimate consumer and business demand. On a more abstract level, financial historians rekindled discussions over whether the new crisis might precipitate a change in the dollar-dominated global monetary order, similar to the Bretton Woods accord toward the end of World War II.

“I wouldn’t rule out anything at this point,” Markus Brunnermeier, a Princeton University economics professor who has advised the International Monetary Fund, Federal Reserve Bank of New York and European Systemic Risk Board, told CoinDesk in late March.

Stephen Cecchetti, who headed the monetary and economic department at the Bank for International Settlements in Basel, Switzerland, in the early 2010s, articulated a key concept that has lurked in the bitcoin market commentary ever since: In times of deep turmoil, the presumption of central bank independence is largely ignored, allowing money printing to finance government budget deficits racked up due to emergency relief spending.

“The central bank has to be a part of the war machine,” Cecchetti, now a professor of international economics at Brandeis University, told CoinDesk.

The dynamic helps explain why bitcoin has been swinging alongside traditional markets based on the on-again, off-again talks in Washington over a new government-funded stimulus package.

Some 10 months after the coronavirus pandemic first started to infect global markets and the economy, the Federal Reserve is still using freshly printed (electronic) money to buy U.S. Treasurys and government-backed mortgage bonds, currently at a rate of $120 billion a month.

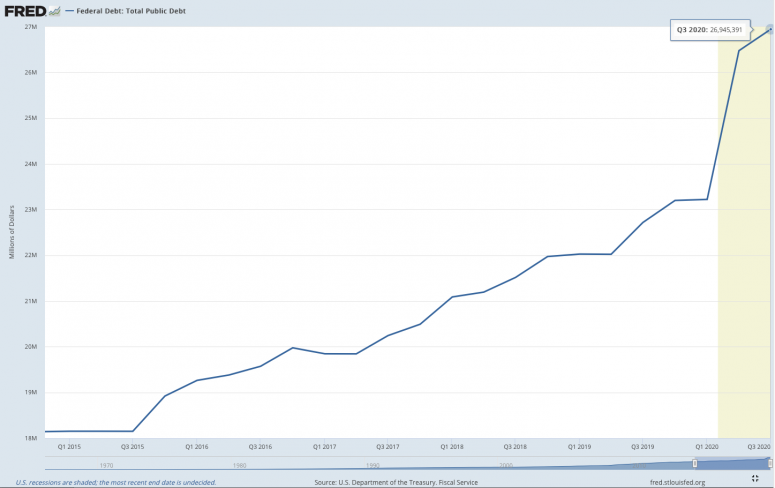

In doing so, the central bank is indirectly financing the U.S. government’s budget deficit, which surged to a record $3.1 trillion in the fiscal year ended Sept. 30, more than twice the prior record of $1.4 trillion set in 2009. The Congressional Budget Office has forecast a record $3.1 trillion for the current fiscal year, remaining above $1 trillion every year through 2030.

U.S. government debt held by the public, which started 2020 at an already-lofty $23 trillion, has now surged to about $27 trillion, and some bond-market analysts predict the Federal Reserve might need to keep monetary policy unusually loose for years to come – just so the Treasury Department can afford its interest payments.

The dynamic, set in motion in March and April, continues to prompt more of those phone calls to crypto startups from Wall Street. On Tuesday, Bank of America published a survey of fund managers showing that “long bitcoin” was one of the most “crowded trades” in global markets, along with “long tech” and “short dollar.”

“Over the course of 2020, many institutions have started to endorse bitcoin,” according to a report Tuesday by the cryptocurrency analytics firm Coin Metrics. “One of the most commonly cited reasons for this change of tune is the growing narrative that bitcoin could serve as a good hedge against inflation.”

With bitcoin prices now above $19,000, the story doesn’t seem to be going away.

– Bradley Keoun

Bitcoin watch

After testing investor patience for three weeks, bitcoin has finally crossed above $20,000 to reach fresh all-time highs.

The No. 1 cryptocurrency by market value jumped over the key psychological threshold during the early U.S. trading hours, surpassing the previous peak price of $19,920 recorded Dec. 1. At the current price of $20,374, bitcoin is up 5.4% over 24 hours, according to CoinDesk’s Bitcoin Price Index (BPI).

Breaking above $20,000, which represented a significant hurdle in the mindset of most traders, is entirely new ground for bitcoin and opens the doors for a climb to $100,000 over the course of 2021, according to some analysts.

While bitcoin is now up over 180% on a year-to-date basis, gold has added just over 22%. Bitcoin, often touted as digital gold, has decoupled from the yellow metal this quarter with a more than 80% rally. Meanwhile, gold has suffered a 1% drop, with investors pulling money out of exchange-traded funds.

– Sebastian Sinclair and Omkar Godbole

Token Watch

Monero (XMR): Privacy-focused cryptocurrency surges to new 2-year high.

XRP (XRP): Ripple lands former JPMorgan Treasurer (and Jamie Dimon lieutenant) Sandie O’Connor as new board member.

Ether (ETH): Options action subsides in December.

What’s hot

Japan’s SBI Financial acquires institutional crypto desk B2C2 (CoinDesk)

Cboe Global Markets plans to launch cryptocurrency indexes in 2021, in licensing partnership with CoinRoutes (CoinDesk)

London-based Ruffer Investment allocates 2.5% of $620M multi-strategies fund to bitcoin (CoinDesk)

Riot Blockchain, Nasdaq-listed bitcoin mining company, pilots new liquid-cooling technology in Texas to test solutions for difficult (hot) ambient conditions (CoinDesk)

CEO of bitcoin mining startup Layer1, Alex Liegl, resigns as part of settlement between founders, just weeks after he was named to the Forbes 30 Under 30 List for 2021 (CoinDesk)

Silk road’s Ulbricht being considered for pardon by Trump, per Daily Beast report (CoinDesk)

Becoming a self-sovereign: How to set up a Bitcoin node, with Lightning (CoinDesk)

Analogs

The latest on the economy and traditional finance

U.S. congressional leaders say they are closer to bill for coronavirus relief, year-end spending (WSJ)

Massachusetts securities regulators to file complaint against Robinhood (WSJ)

Bets on world of negative interest rates end with capitulation (Bloomberg)

U.S. government-owned mortgage-finance companies Fannie Mae, Freddie Mac slump as Treasury Secretary Mnuchin rules out letting them exit federal control, citing need to maintain consumers’ access to home loans (Bloomberg)

Billionaire investor Warren Buffett tells CNBC that Congress should extend the U.S. government-funded Paycheck Protection Program to help small businesses affected by coronavirus restrictions (Bloomberg)

Software firms allegedly breached by suspected Russian hackers, including SolarWinds and FireEye, have seen their share prices nosedive, hitting private-equity stakeholders Silver Lake, Blackstone (Reuters)

Iranian oil exports rise as Tehran circumvents sanctions, finds new buyers including China (WSJ)

MSCI, the investment research firm and stock-index provider, said it will delete 10 Chinese companies from global indexes after the U.S. imposed restrictions on their ownership (Nikkei Asia Review)